To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Category: Weekly Detail

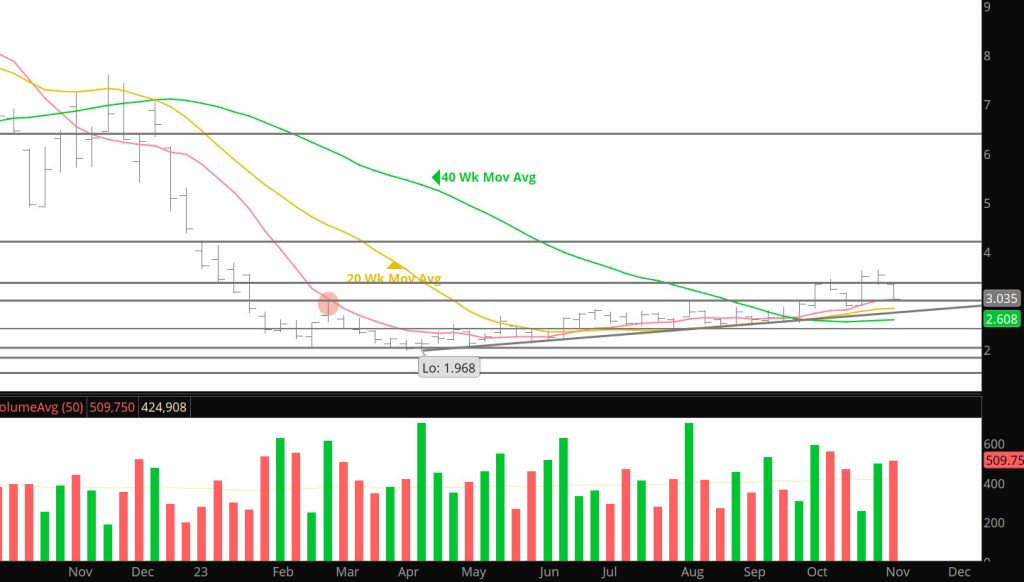

Prices Retain Most of the Premium

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Nov Well Bid Into Expiration

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Break Out Confirmed — So Far

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Headed For The Q4 Rally

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

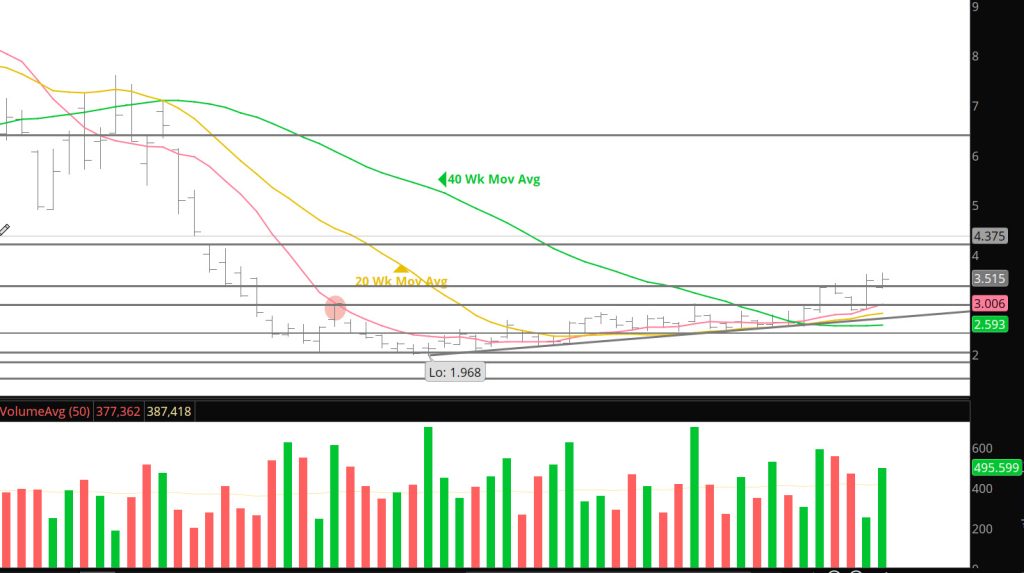

Headed To Bias Determination

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Large Premium In Nov Over Oct

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

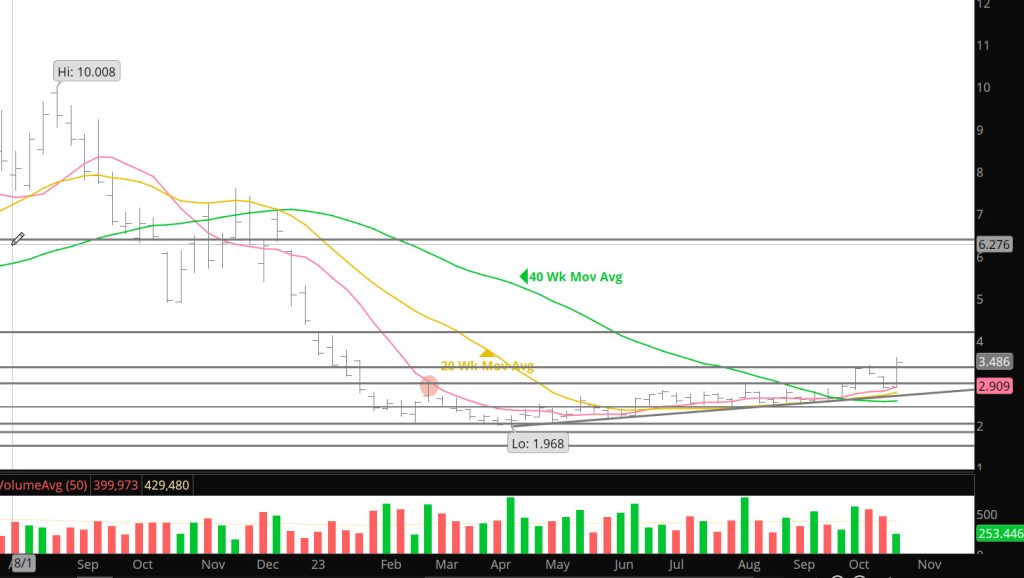

Gap Open For Prices

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Stalls At High End of Range

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

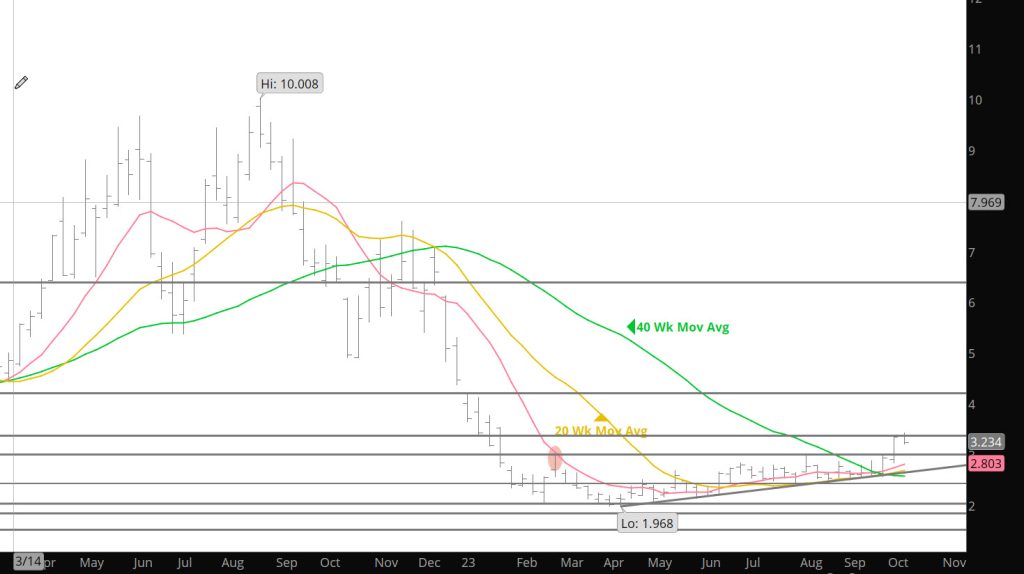

Gas Continues Recent Behavior

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.