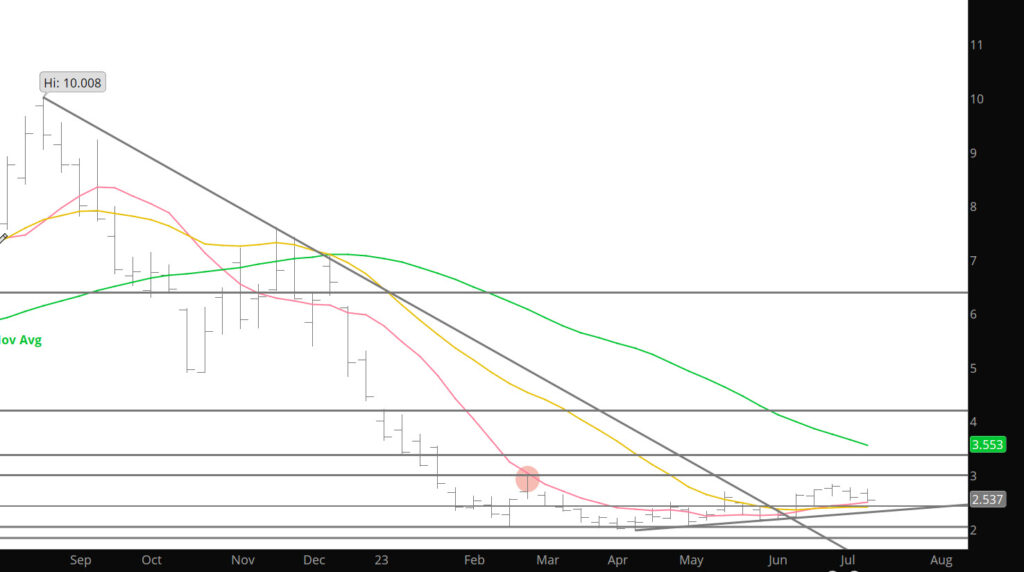

The two day rally failed at the start of the week fell a little short of last week’s high ($2.750 v $2.793), which was lower than the previous week’s high and the rally gains were quickly forfeited. With volume increasing the prompt tested last week’s low but held just above $2.536 ($2.539)…lower trade for a third straight day validated last week’s ideas of lower trade as the post – Independence Day decline was extended to $2.492.

The historically consistent seasonal decline from a late June high (measuring from the 06/20 recovery high of new prompt August), was extended to $.336 or just about 12%. That is a little more than the three and five years average declines, a little less than the average of the last ten years. While the memory of last year’s rocket ride from the post – Independence Day low (from an 07/05 low of $5.325 August ’22 rallied to a 07/26 high of $9.752) is still fresh, the recent price action is more typical of July trade. Declines should be extended a little further before sufficient sponsorship is uncovered to lift August to a somewhat higher expiration. History suggests that over the years August has settled lower than July far more often than not, but August has been higher in each of the last three.