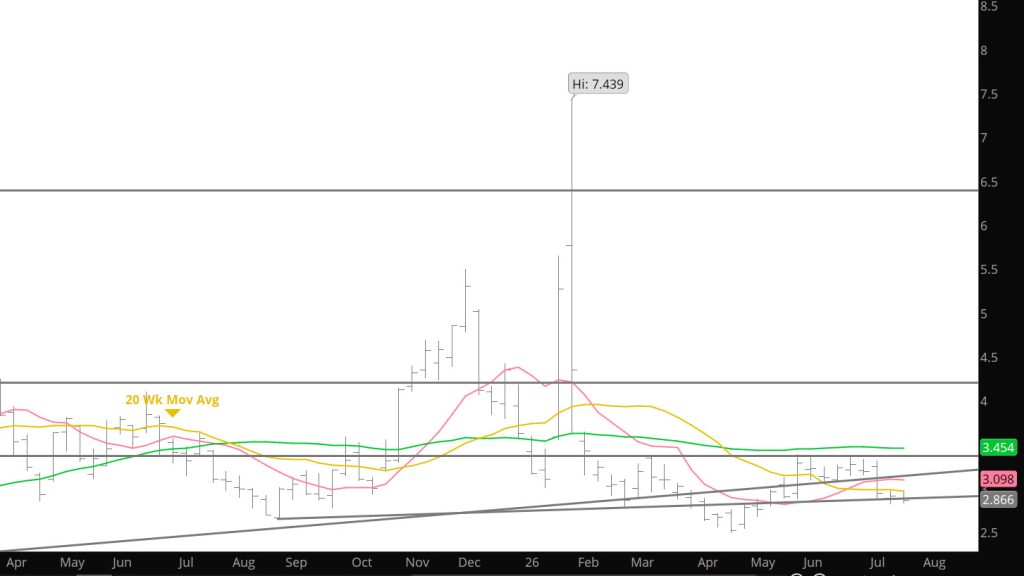

Soon to expire August, which rallied from last week’s low of $2.823 to$ 2.991, traded back to back tight weekly ranges (last week $.145 from low to high…the tightest weekly range in memory, this week $.160) but was the only contract month to end the week with a loss. The consensus of technical indicators, which remained neutral (with a fluctuating bias) for the entire second calendar quarter, is negative for a second week.

The weekly MACD, our primary “lagging” indicator, which confirmed a negative calculation last week, is negative for a third week. The daily MACD, the daily and weekly RSIs are negative and are not yet giving extremely oversold warnings. Market internals are neutral. Average daily volume fell a little as August traded between support and resistance.