To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Category: Weekly Detail

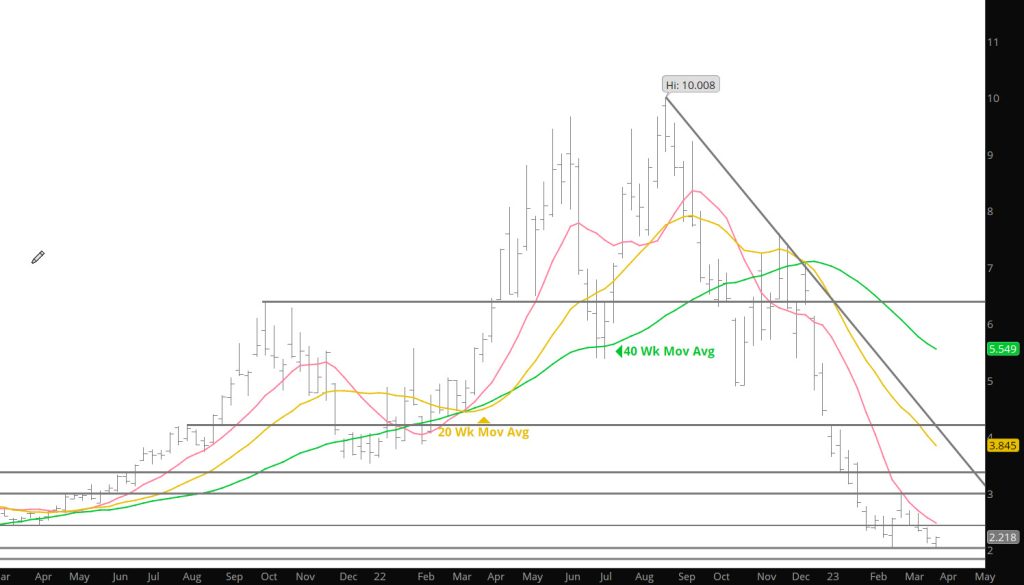

Lower Weekly Close Suggests Continued Weakness

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

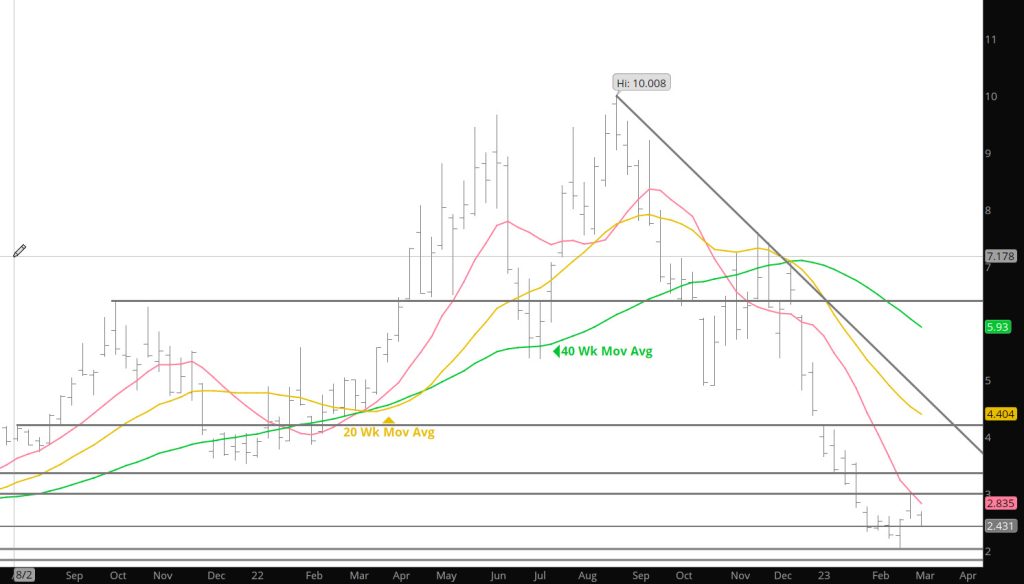

Declines Test Strong Support Zones

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Bullish Move But Caution

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Market Bias Maybe Changing

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Bears Continue to Rule

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Further Evaluation

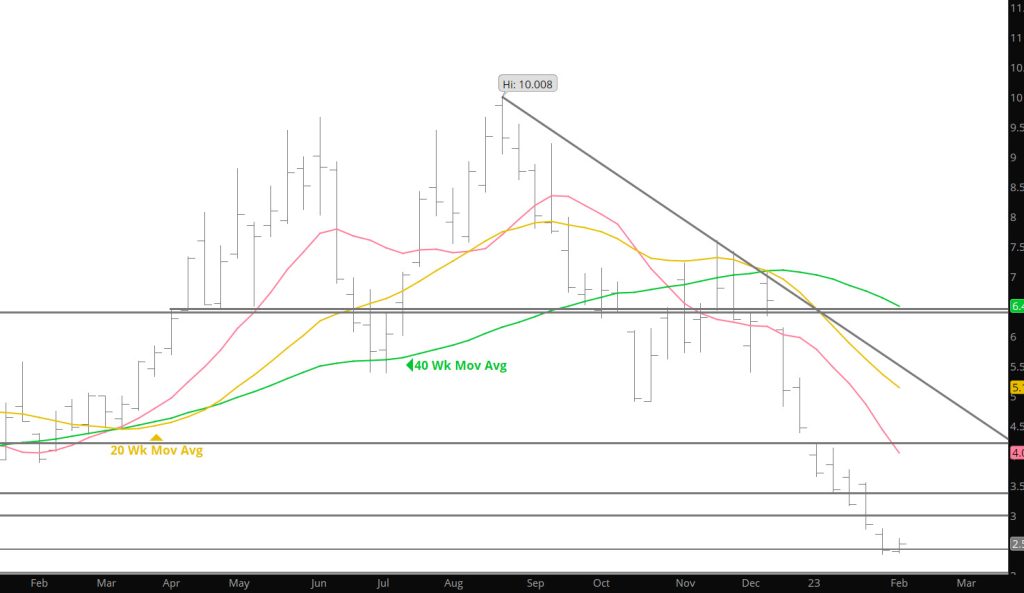

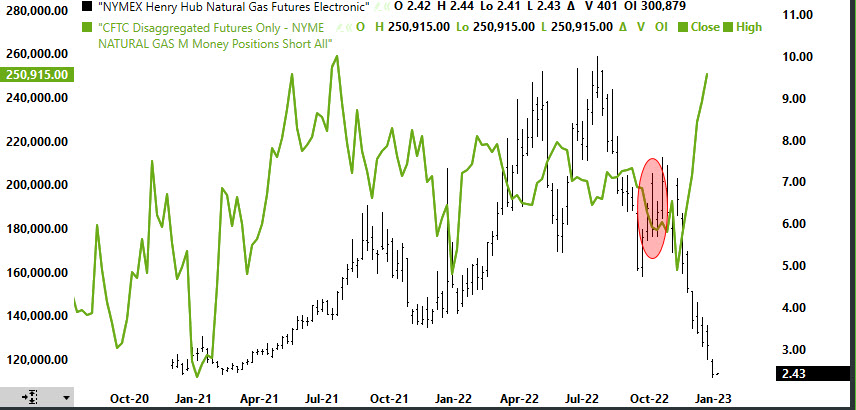

Feeling better and capable of bringing thoughts together I offer this Weekly updated for this week’s action. It may be that the “inside” week (concluding last week) is just a pause for an astronomic oversold gas market, but I beginning to think that the downside momentum developed since those bearish momentum divergences way back in August is finally exhausted or getting extremely close to it.

The gas market fueled by speculative fervor (previously discussed Managed Money position short gains) characteristically take trends further than what is sustainable.. Prices did that in June ’20 when there were projections of a prompt price under a dollar then it did that back in last August when prompt September fleetingly visited the rarefied air over $10 for the first time since the hedge fund inspired run in the spring and summer of ’08. Last summer’s correction was quick and efficient.

My view is that the gas market has just begun the basing process and its early, only one week removed from trading a lower low, but most technical objectives have been met and then some. While the consensus of technical indicators is still solidly negative, the extreme state brought by the most recent phase of the decline (from the November/December highs) moderated a bit. The weekly RSI are still extreme and the RSI has ended in its EXTREME zone for the last six weeks…it has not done that since the decline from the ’08 high. Being extremely oversold does not mean that an indicator can’t get more oversold (witnessed that over the last few weeks), but that’s not the history of the purely mathematical indicators. More interesting is something of a change in the market’s internal characteristics during the past week. Volume has been increasing as the market fell that’s what is supposed to happen if a trend is to continue, but last week the volume starting increasing as the market rallied. On Tuesday 619,703 contracts traded…the highest daily volume since June 14th. The range traded that day was $1.881…the range traded on 02/07 was $.192. What I expected to see the next day was that open interest had declined indicating that a bunch of shorts had covered an existing position but that did not happen. Rather, open interest increased 7,362 contracts– that could show a strong indication that more than enough new buying came into the market to offset the amount of short covering. That is the first technical positive suggestion from market internals since the fall.

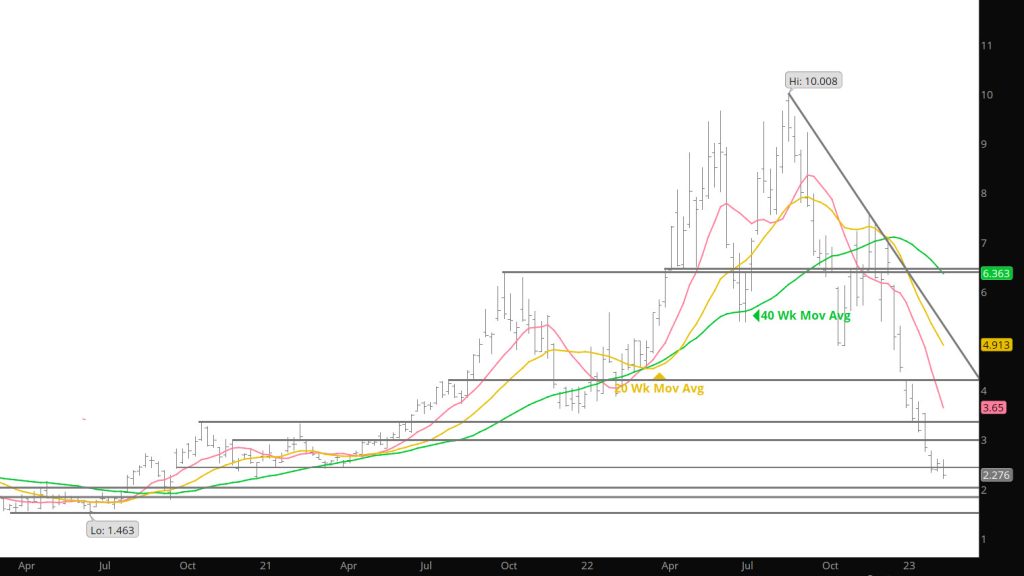

Major Support: $2.533, $2.422, $2.238

Minor Support:

Major Resistance$3.536, 3.595, $3.63, $3.789, $4.128, $4.22-$4.39, $4.75-$4.825, $4.948

Important Change May Be Starting

Fell victim to a serious sinus bug late last week and with the headaches — will not try put the market in perspective. Will try tomorrow or Tues

Bull’s Stand Aside-Humor Will Come

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Bearish Technical Indicators Continue

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.