To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Category: Weekly Detail

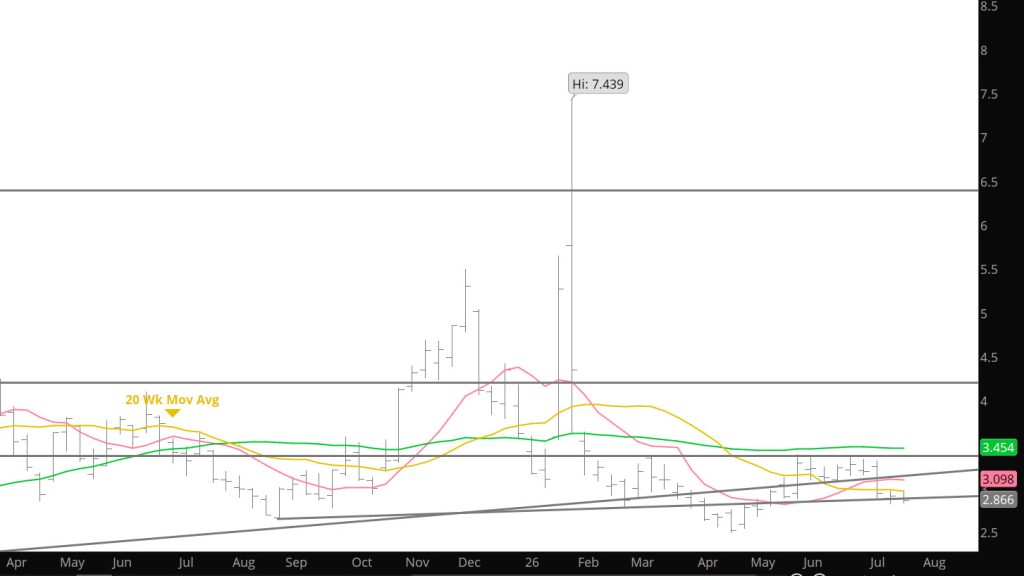

Operating In Tight Range

Weekly Continuous

After losing $.256 a week ago August closed $.029 lower, while trading a total range for the week of $.145 that may suggest at least a temporary loss of downside momentum. August gas spent six trading days testing the same zone that provided resistance during the first half of May and then support for expiring June just after Memorial Day . Volume during the last five of those six days was lower than the corresponding day the week before…no technical surprise that prompt gas held the support. As a rule, a volume increase is required to overcome the bids at a defined support zone. August traded an outside day reversal on Thursday and posted a low daily close of $2.858…the lowest daily close since then prompt June closed at $2.843 on 05/12. If August was going to breakdown, it missed a good chance, but the sufficient offers clearly were not present.

On a daily closing basis, prompt gas closed between +/- $2.550 and $2.850 for twenty six days between April 1st and May 13th (there was one close higher, three lower during that period). That zone was tested this week…expect it to continue to present daily closing support but also that it will be retested during late July, August and early September. Note that September is currently $.035 discount to August. A year ago on 07/17 September closed $.034 premium.

Following the seasonal pattern during July…and particularly the period bracketing Independence Day, August was expected to trade a low between the 10th and 20th…this week’s low traded on 16th and brought the early July decline to 18% (vs a five years average of 18.9%). While as mentioned in previous editions, there have been years when August faded for its entire tenure as prompt, far more often a post – holiday mid – July low precedes a rally to test resistance. Expect the zone between $3.10 and $3.15 is a likely target before a fade into contract expiration.

A year ago August ’25 traded a temporary oversold, seasonal low on 07/09 and then rallied to retrace a little less than 50% of the decline from the Q2 high, tested similar resistance then failed. Expect seasonal pressure to ebb and flow weighing on the entire maturity curve for another sixty days. The average of the last twenty declines from Q2 highs is 31.6%…which would suggest some likelihood of a test and possible undercut of the April low. Full maturity of the annual cycle will occur in 4 – 5 weeks, or roughly during the last week or so of September’s tenure as prompt…which will also be full maturity of the short – intermediate term cycle measured from the April low. The best guess is that the gas market will feel seasonal pressure into that late August/early September period and the period bracketing Labor Day (which is 09/07 this year).

The consensus of technical indicators, which remained neutral (with a fluctuating bias) for the entire second calendar quarter ended the week negative for the first time since just following the failure at the January high. The weekly MACD, our primary “lagging” indicator, that had remained positive for eight weeks rolled over. The daily MACD and weekly RSI are negative and are not yet giving extremely oversold warnings. Market internals which were neutral with the suggestion of a price negative bias last week improved a little. Average daily volume (which accelerated significantly a week ago as prompt gas fell hard) and the highest since the two weeks leading into and of the week of the March high, dried up as August traded a lower low…a technical positive.

Open interest increased 21,500 contracts as August edged lower…my guess is that increase can be attributed to short sellers getting a little too far out over their skis. Thursday’s total was 1,672,716 total contracts outstanding. The last time open interest was as high, 1,676,152, was week ending 05/29. The time before that, 1,680,104, was the week immediately preceding the January low. Those are the high week ending totals since last October…both accompanied a turn in the market.

Major Support: $2.640-$2.57

Minor Support/Resistance : $2.87-$2.84, $3.16-$3.148, $3.136, $3.02-$2.97

Major Resistance: $3.35, $3.486-$3.494, $3.567, $ 3.736

Storage Release Breaks Old Support

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Range Trade Supports a Break Eventually

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

New Prompt — Same Range — So Far

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Nothing Technically New

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Not Much To Write

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Seasonal History Remains

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Bias Change Receives Some Confirmation

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.

Still Churning

To read The Daily Call you must be a subscriber (Current members sign in here. ) Start your subscription today.