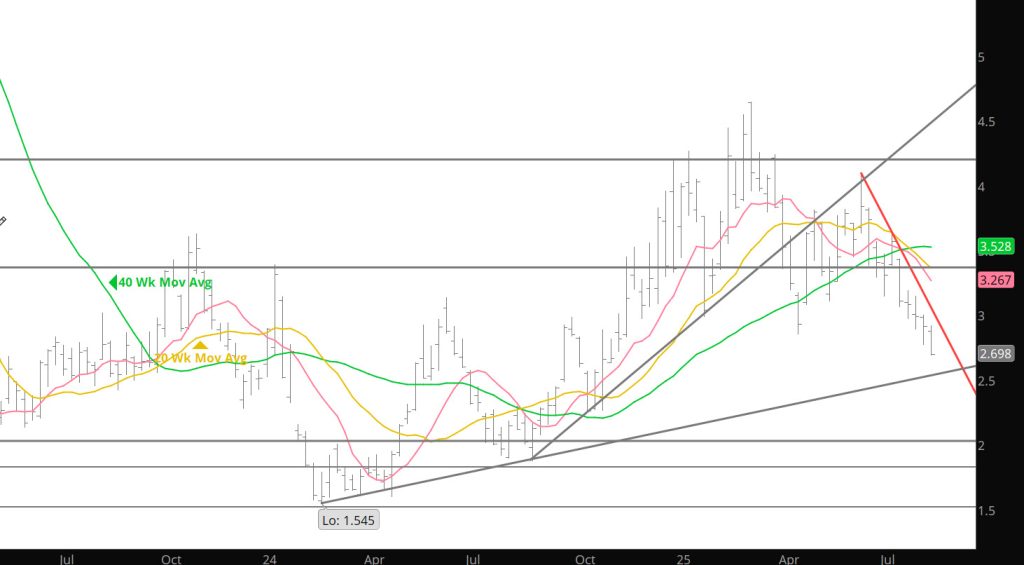

The collapse continued last week as prices extended the declines though some support trend lines and previous month lows. The violated trend line now becomes ascending resistance, as the dominant near term technical factor. Given soon to expire September’s weakness into the week’s close the trend line is likely to contain any near term short covering rally as well as any early sponsorship for October (which closed at $2.800, $.122 premium to September and also below the coming week’s value of the trend line). Given the violations of trend line support during the last two weeks and prompt gas entering the seasonally weak period during the coming week (Labor Day falls on September 1st this year), the upside prospects for the expiring contract and new prompt October seem low.

Historically, the days leading into and following Labor Day has been one of the most consistently price negative periods all year. Since I first noticed the tendency, declines were and continued to be consistently in double digits. When they weren’t (which was rare) I learned from history, that when the markets that fail to decline when they are supposed to (based on historical norms) are likely going to go up and less than average declines tend to precede robust Q4/Q1 rallies. In ’23 the decline was 12.5%. The entire Q4 rally was a little more than a dollar counting the premiums awarded to the November and December contracts. The Q4 peaked on 10/31/31 at $3.630, 70% higher than the pre Labor Day low. A year ago the Labor Day decline was short and measured only 7.4%. During the period that immediately followed (about three weeks) prompts October and November rallied $.894. You might remember that the rally that began from the pre Labor Day low was not exhausted until early March with the prompt price 164% higher.